DigitalOcean Crushed the Quarter and Raised Guidance Because: AI.

The middle layer is starting to matter.

DigitalOcean crushed 1Q26 and the stock is up $40 (37% midday) because AI ARR was up 221% to ~$170M – now 17% of the mix versus 5-7% a year ago – and management expects that to drive 2027 top-line growth of ~50% versus 26% growth for this year.

Their website (now) proudly proclaims them the “AI Native Cloud” (from the “Inference Cloud” the other day). Their numbers are catching up to their tagline(s).

The arc.

This arc began with their acquisition of Paperspace in 2023. Despite (profound) hiccups early, (new) management (e.g., CEO Paddy Srinivasan, who joined two years ago), took the company from an option on GPU cloud and patched up fundamentals, through AI tailwinds in 4Q25, to an increasingly more focused play on AI infra.

The fundies.

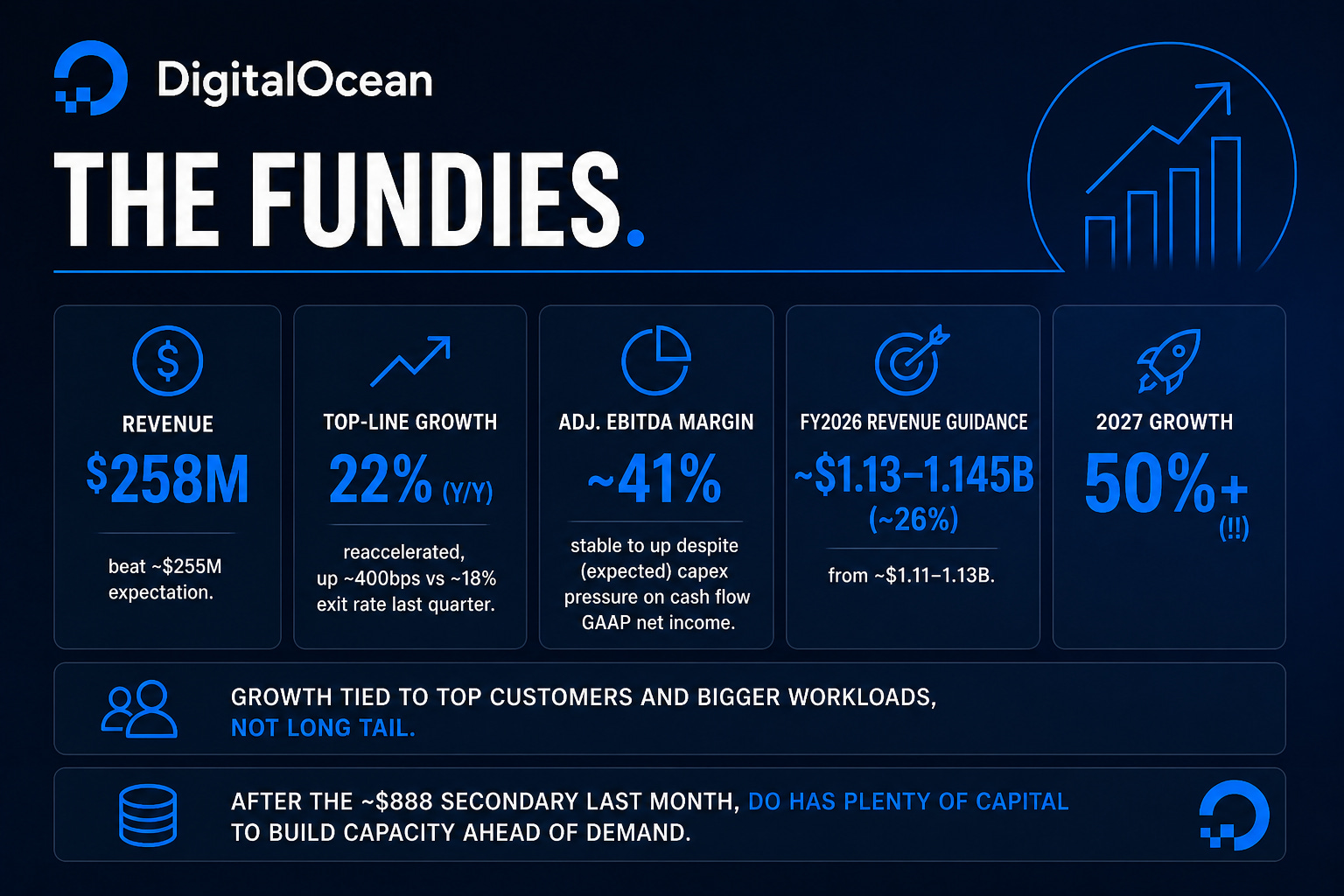

Revenue $258M beat ~$255M expectation.

Top-line growth reaccelerated to 22% (y/y), up ~400bps vs ~18% exit rate last quarter.

Adjusted EBITDA margin was ~41% (stable to up) despite (expected) capex pressure on cash flow and GAAP net income.

FY2026 revenue guidance to ~$1.13-1.145B (~26%) from ~$1.1B.

2027 growth now targeting 50%+(!!)

Notably, growth was tied to top customers and bigger workloads, not long tail. And after the $800M+ equity offering in March, DO has plenty of capital to build capacity ahead of demand.

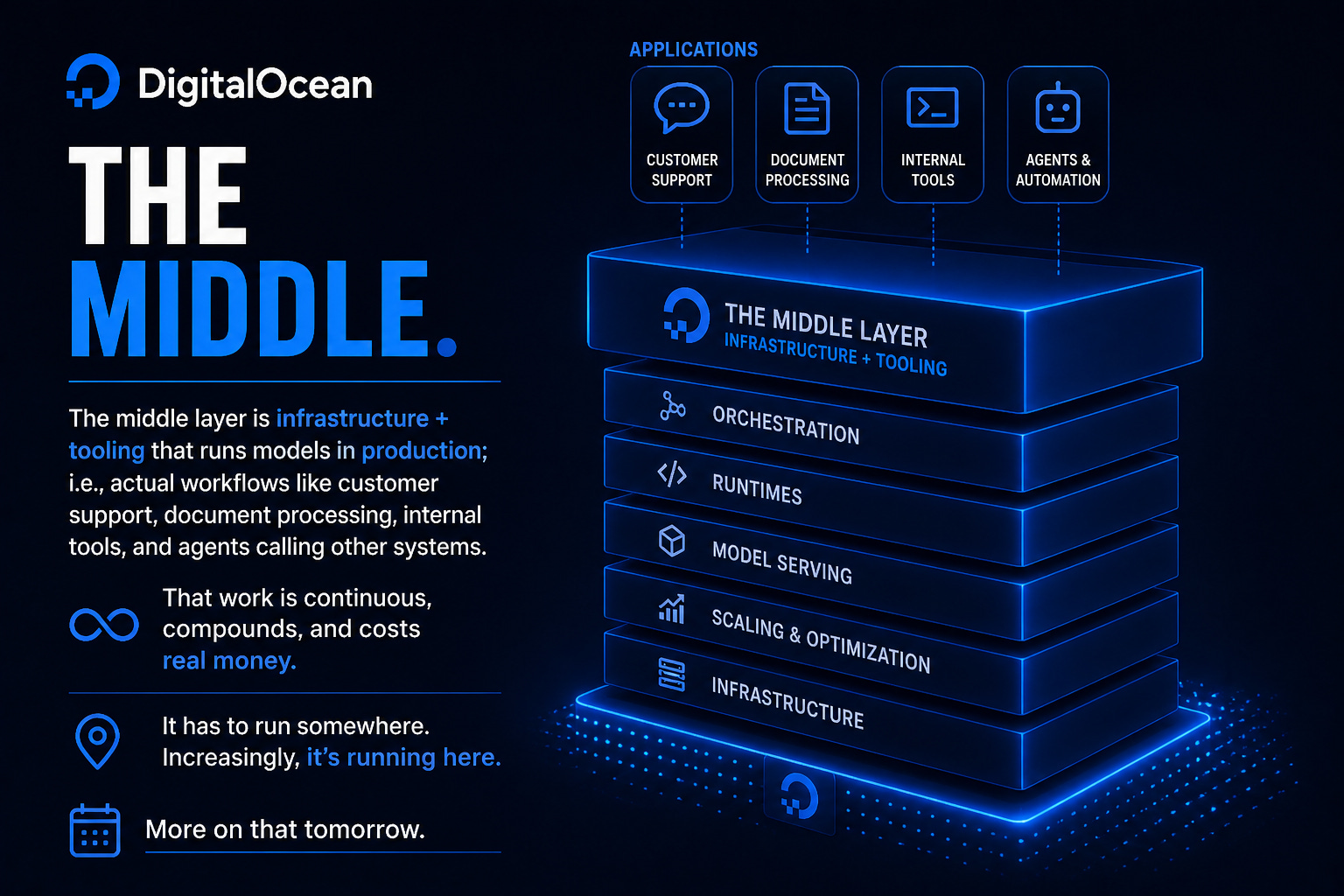

The middle.

The middle layer is infrastructure + tooling that runs models in production; i.e., actual workflows like customer support, document processing, internal tools, and agents calling other systems. That work is continuous, compounds, and costs real money.

It has to run somewhere. Increasingly, it’s running here.

More on that tomorrow.

DO’s shift, From the Porch.

This is what exercising DO’s GPU option looks like.

Disclosures: I was in and out of DOCN a few years ago around $40; that was stupid. I also didn’t buy DOCN when I first wrote DigitalOcean’s GPU Option (parts 1 and 2) last year. I also didn’t buy it when they reported a blowout 4Q25 earlier this year despite a stock dip based on irrational margin compression fears. TLDR: do what I say, not what I do.