1Q26: Proof of AI.

Weekend reading, From the Porch: Show me the receipts.

Six infrastructure stocks reported or posted big news this past week. Most beat estimates, but the stocks moved in completely opposite directions. The signals were confusing and the noise was loud.

But none of it changed the thesis.

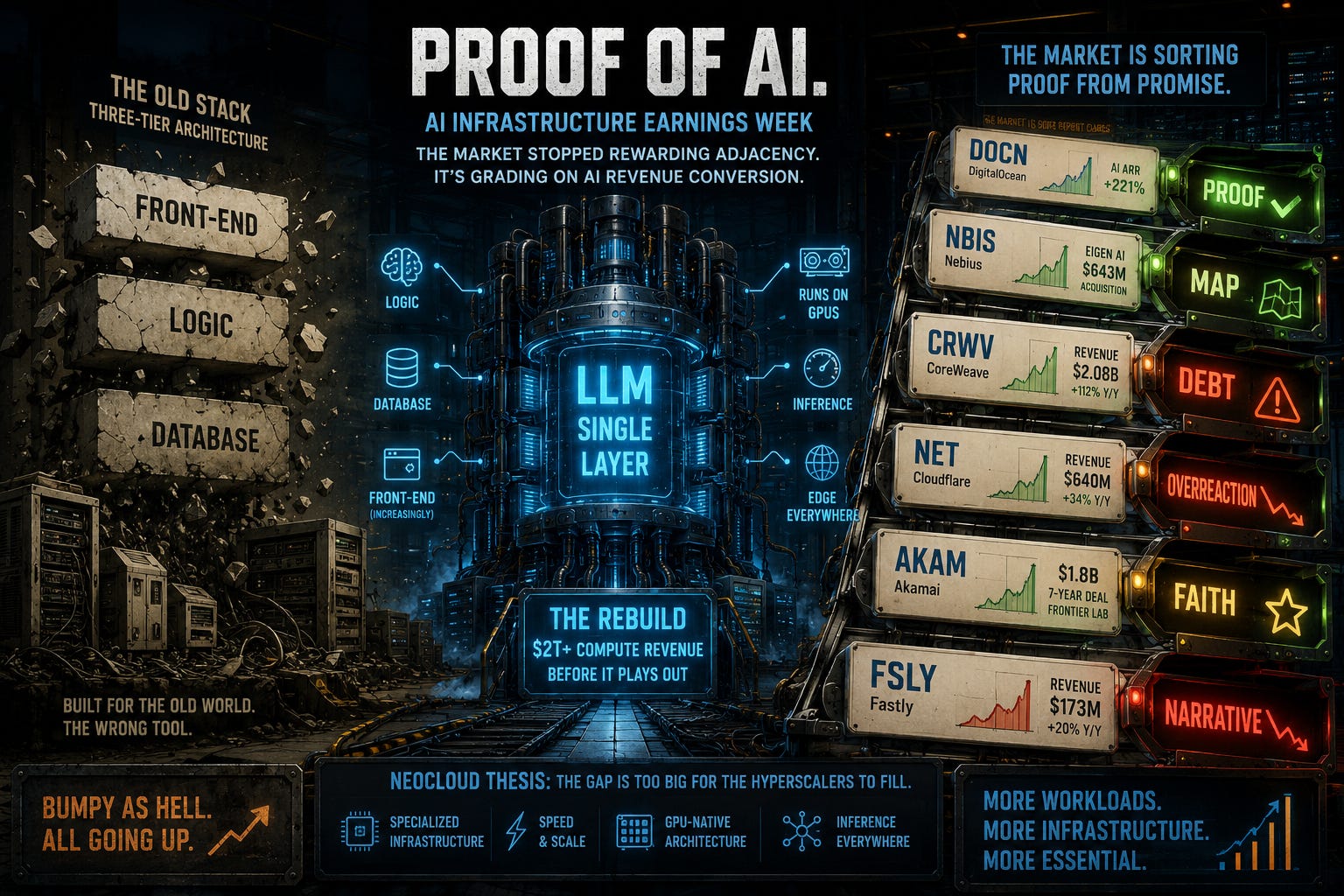

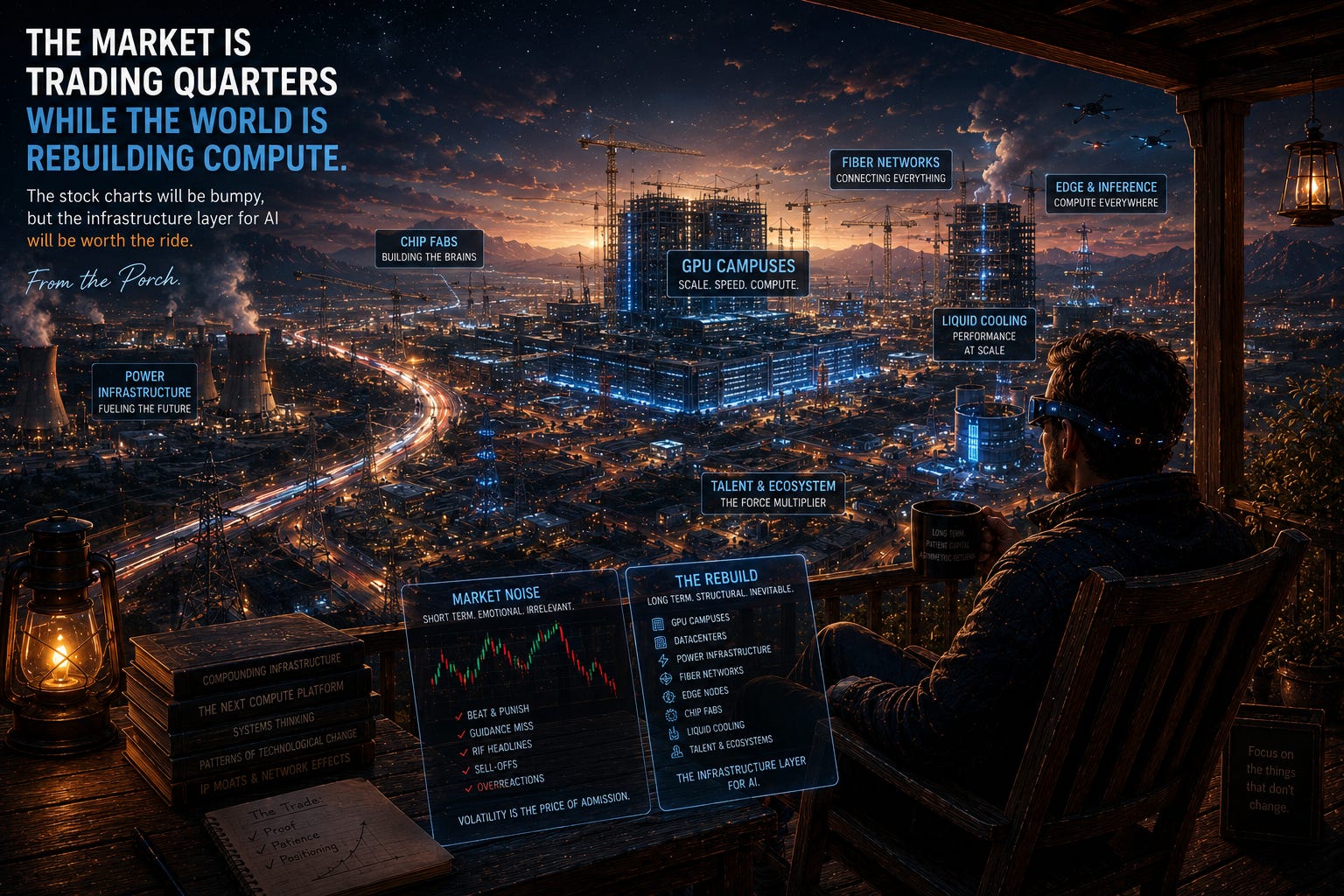

TLDR: the world’s computing infrastructure has to be rebuilt (not just upgraded) because AI compresses the old stack. The traditional three-tier architecture (front-end, logic, database) is collapsing into a single layer. The LLM is the logic and the database and (increasingly) the front-end. And that thing runs on GPUs. Every server rack, data center, edge node built for the old world is the wrong tool. The bill to rebuild it is $2T+ in compute revenue before it plays out. And it’s not all going to AWS, GCP, and Azure — which is why the neocloud thesis exists, and why I’ve been writing about it since 2024.

Last week, the market started grading the rebuild era more broadly. It was looking for proof. Not just quarterly results, AI exposure or proximity, or new taglines on websites announcing AI branding. Here’s what the report cards looked like — and what to do.

The Honor Roll.

DigitalOcean (DOCN) beat and raised again (again). Revenue was $258M (+22%) and AI customer ARR (+221%) is now 17% of the total mix. They guided for 26% growth this year and, perhaps audaciously, 50%+ next year. The stock gapped up 30%+ the next morning.

I’ve been writing about DOCN’s arc for a while now. Here’s the capsule version: three years ago it was a second- (third-?) rate cloud provider losing customers up and down the stack. They bought Paperspace to get into AI in 2023, but their existing business subsequently fell apart. It was ugly: they missed a quarter, restated historicals, lowered guidance, and fired the CEO (and got “rewarded” with a ~50% stock decline to the $20-range). New management, new positioning, three consecutive beat-and-raise quarters later — the numbers are catching up to its (new) “AI Native Cloud” branding. AI ARR is real, it’s growing, and now it’s large enough to move the top line. The market loves its AI story and (even more) its revenue growth acceleration forecast.

This is exactly the middle-layer story to which I keep returning. DOCN is running models. That’s the business.

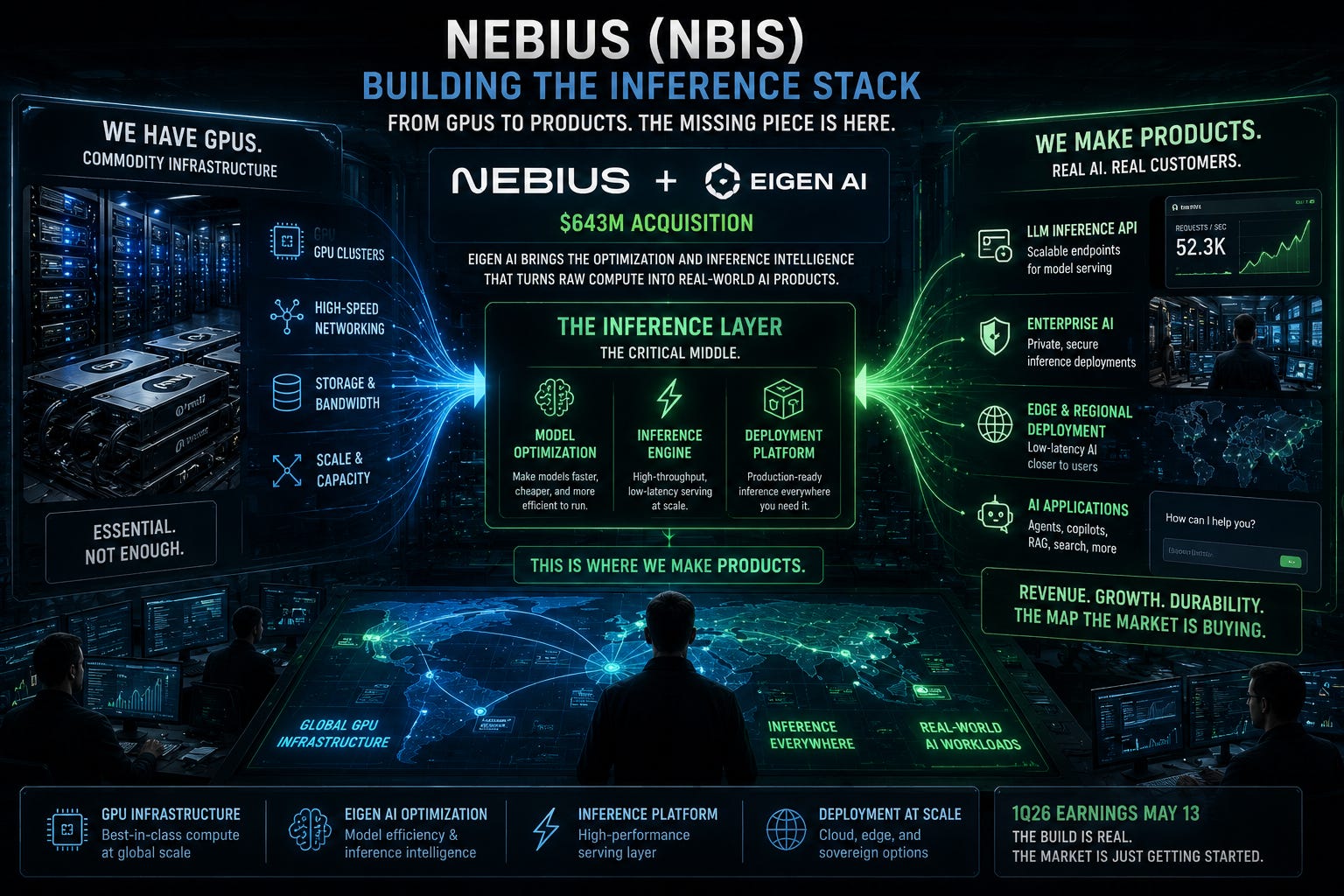

Nebius (NBIS) popped on the $643M acquisition of Eigen AI — an inference and model-optimization company — which I wrote about in detail here. 1Q26 earnings don’t drop until May 13, so this is a pre-earnings pop on deal conviction, not a numbers reaction. (Translation: you’re not done nail-biting.) The market is buying the map: GPU infrastructure + optimization + inference deployment, all in one place.

The Eigen deal fills the exact gap that sits between “we have GPUs” and “we make a product.” This is where NBIS just planted its flag.

The Paradox.

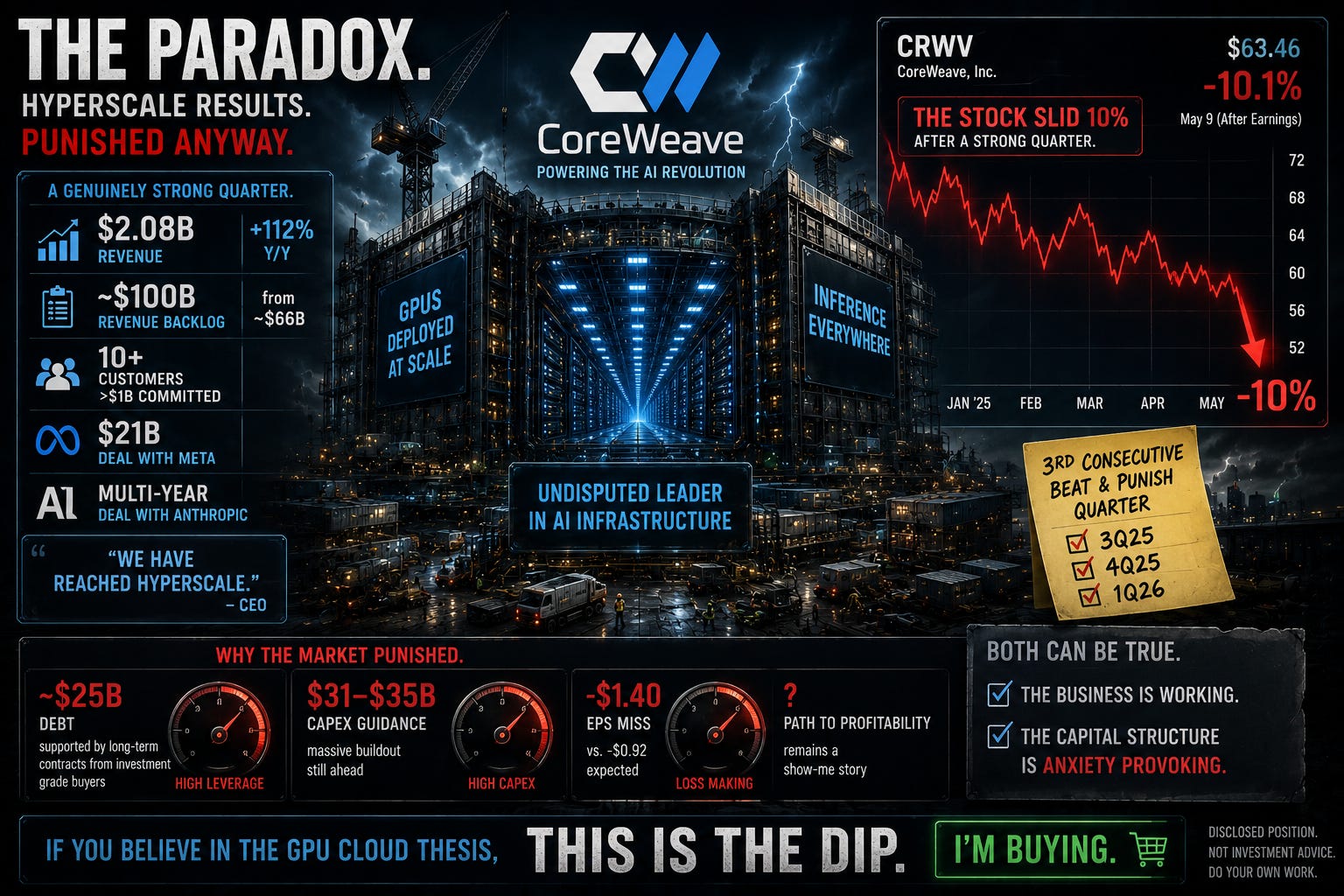

CoreWeave (CRWV) had a genuinely strong quarter. Revenue $2.08B (+112% y/y) beat estimates. Revenue backlog approached $100B (from ~$66B). Ten customers committed to spending more than $1B each. A $21B deal with Meta and a multi-year deal with Anthropic signed in the quarter. “We have reached hyperscale,” the CEO said.

Aaaaand… the stock slid 10%.

This is the third consecutive “beat-and-punish quarter.” It happened in 3Q25 and in 4Q25, and it happened again. The market isn’t doubting the revenue. It’s worried about $25B in debt (notably supported by long-term contracts from investment grade buyers), $31-35B in capex guidance, and an EPS miss of -$1.40 versus -$0.92 expected. And the market evidently concluded that CoreWeave’s path to profitability remains a show-me story.

My view hasn’t changed: CRWV is the undisputed leader in AI infrastructure. Its capital structure, to be fair, is legit anxiety provoking. But both things can be true. If you believe in the GPU cloud thesis — and I do — this is the dip. I’m buying.

The Weird One.

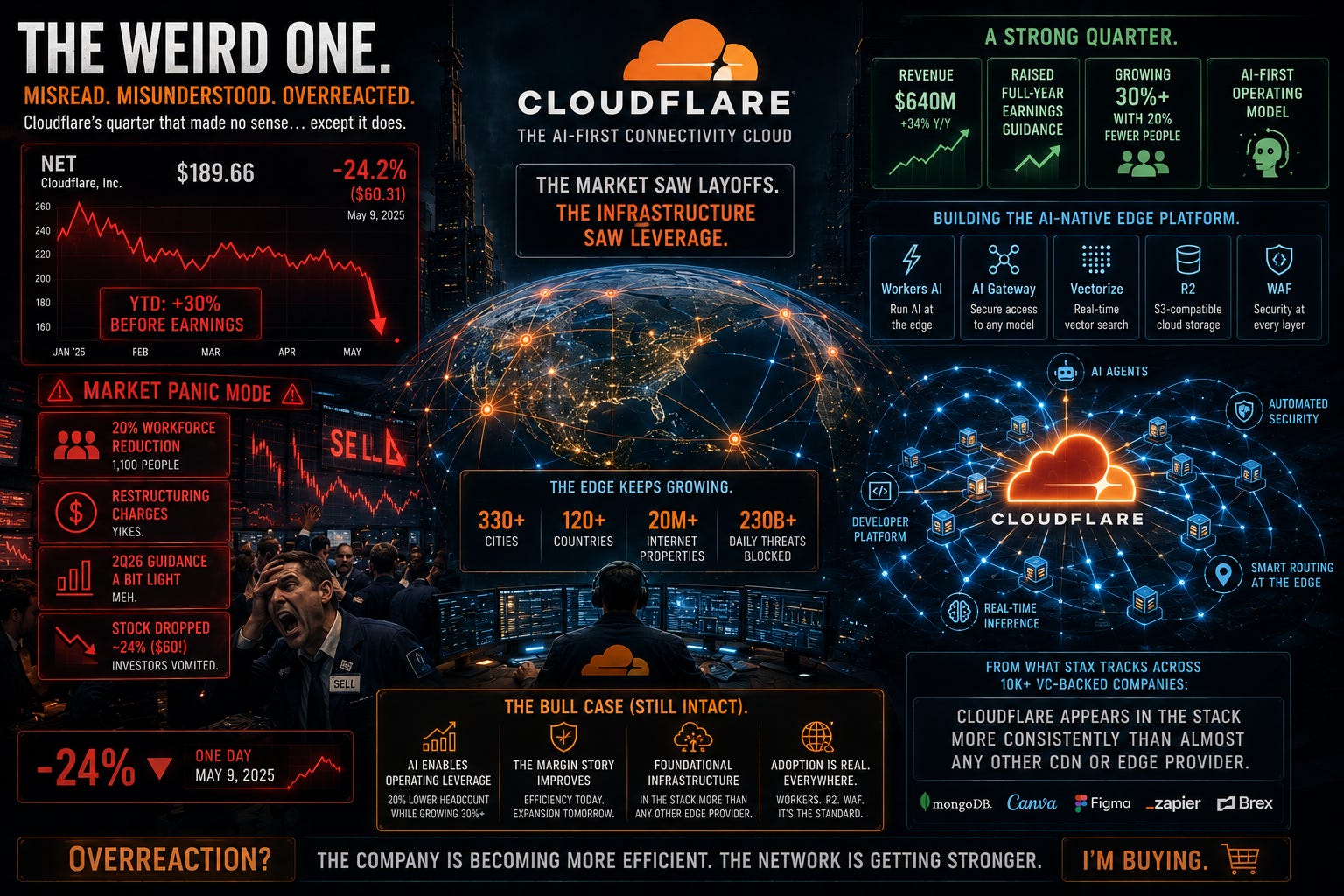

Cloudflare (NET) is the most perplexing of the week’s results. And possibly the most misread.

Revenue was $640M (+34% y/y) and management raised full-year earnings guidance, though 2Q26 guidance was a bit light. They’ve got Workers AI, AI Gateway, Vectorize, etc. – a real product roadmap for the agentic AI era. The stock had been up 30% YTD heading into the print. But with the earnings release they announced a 20% workforce reduction (1,100 people) framed explicitly (and ironically af) as a shift to an “agentic AI-first operating model.”

Aaaaand… yikes. The stock dropped ~24% ($60!) on Friday.

The irony, of course, is that the best example of the bull case for NET is in the layoff announcement. If AI enables them to operate at 20% lower headcount while growing revenue at 30%+, the long-term margin story gets materially better. That should be the signal. Instead, the market saw restructuring charges, a barely-OK guide, and a stock with no room for ambiguity. So, investors dumped (or, more descriptively, vomited) the stock.

From what STAX tracks across 10K+ VC-backed companies: Cloudflare appears in the stack more consistently than almost any other CDN or edge provider. Workers, R2, WAF — it’s everywhere. The underlying adoption is real. And this all looks like an overreaction.

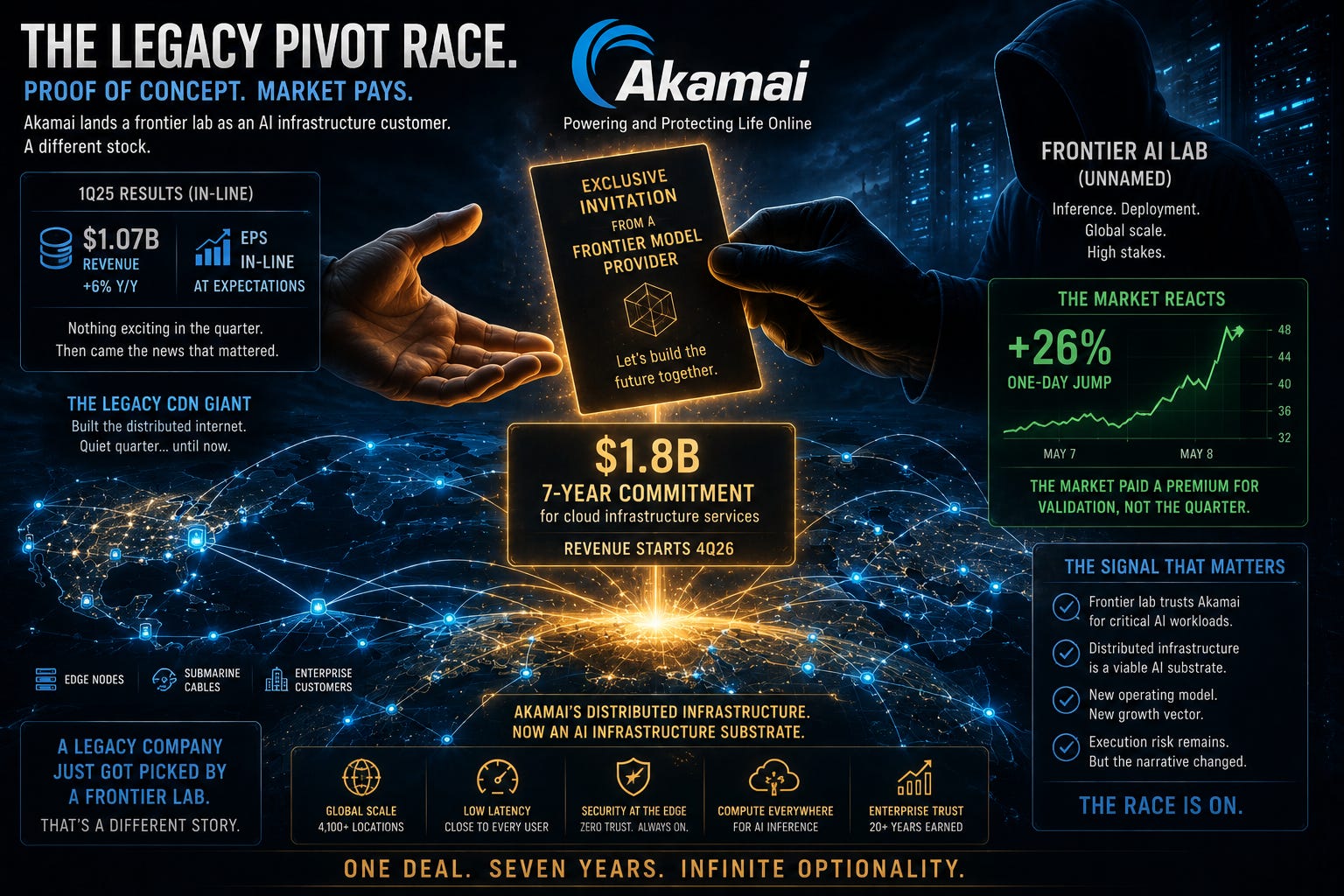

The Legacy Pivot Race.

Akamai (AKAM) reported in-line: $1.07B revenue (+6% y/y), EPS at expectations. Nothing exciting. Then they dropped a $1.8B, seven-year commitment from an unnamed US-based frontier model provider for cloud infrastructure services. Stock up ~26%.

This is the market paying a very high premium for proof of concept — validation that AKAM can land an AI anchor customer at all. The frontier lab – unnamed, presumably (and hopefully?) inference / deployment workloads – is essentially vouching for Akamai’s distributed infrastructure as a viable AI substrate. Revenue doesn’t even start until 4Q26, but the signal mattered: a legacy CDN just got picked by a frontier lab. That’s a different stock than it was for most of the rest of the year during which AKAM lagged its group.

Whether the rest of the business can execute to match the implied new valuation is a separate question.

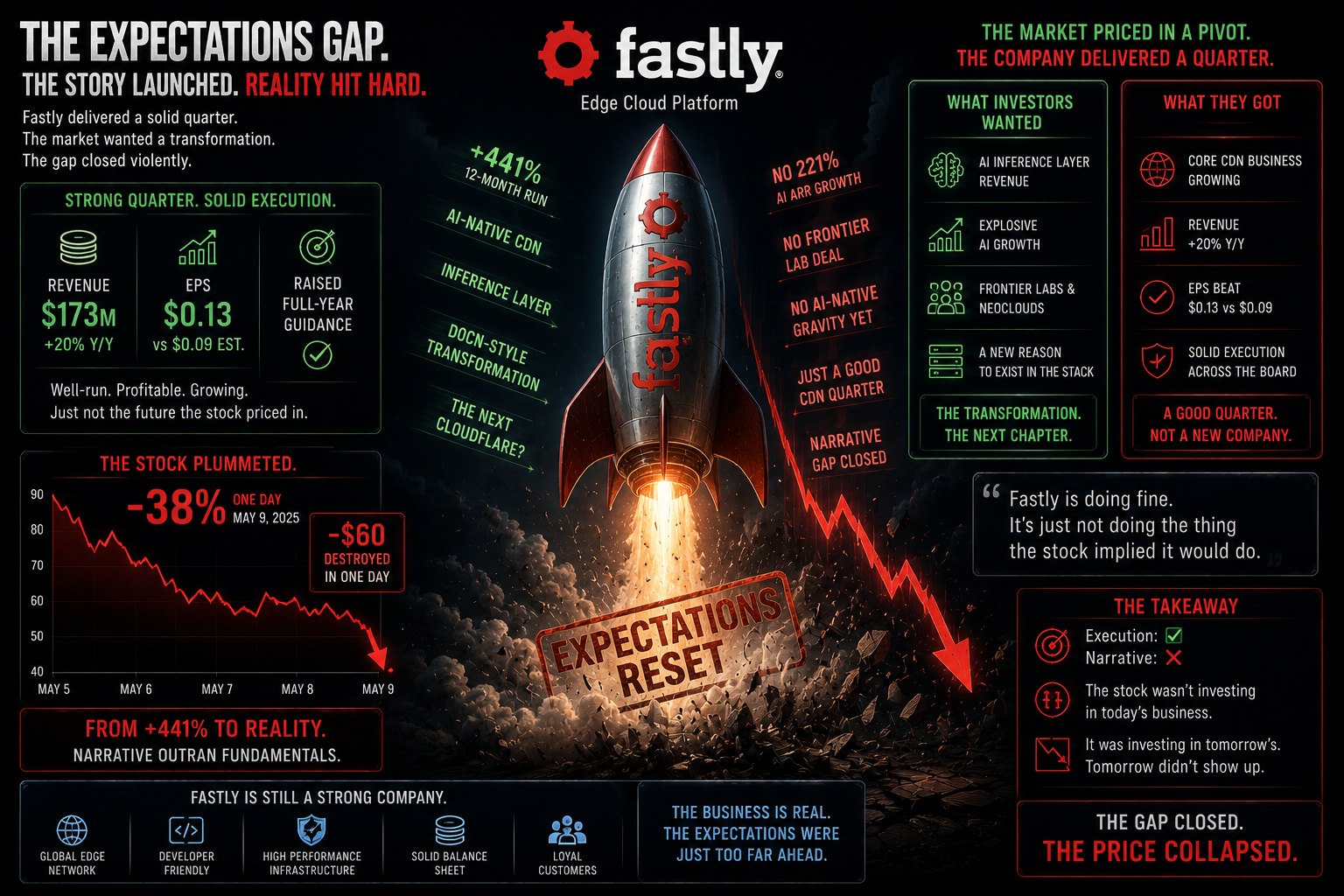

Fastly (FSLY) beat on revenue ($173M, +20% y/y), crushed EPS ($0.13 vs $0.09 expectation), and raised full-year guidance.

Aaaaand… the stock plummeted 38%.

Keep in mind FSLY had run +441% over the prior year on the hope of a DOCN-style AI transformation. The market had priced in a pivot — AI-native product, inference-layer revenue, a new reason to exist in the stack. What they got instead was a well-run CDN quarter. Solid fundamentals. 11% growth in a core business. But not so much AI-specific product gravity. No 221% AI ARR growth. No frontier lab deal.

Fastly is doing fine. It’s just not doing the thing the stock implied it would do. The gap between narrative and reality closed violently.

The Thread.

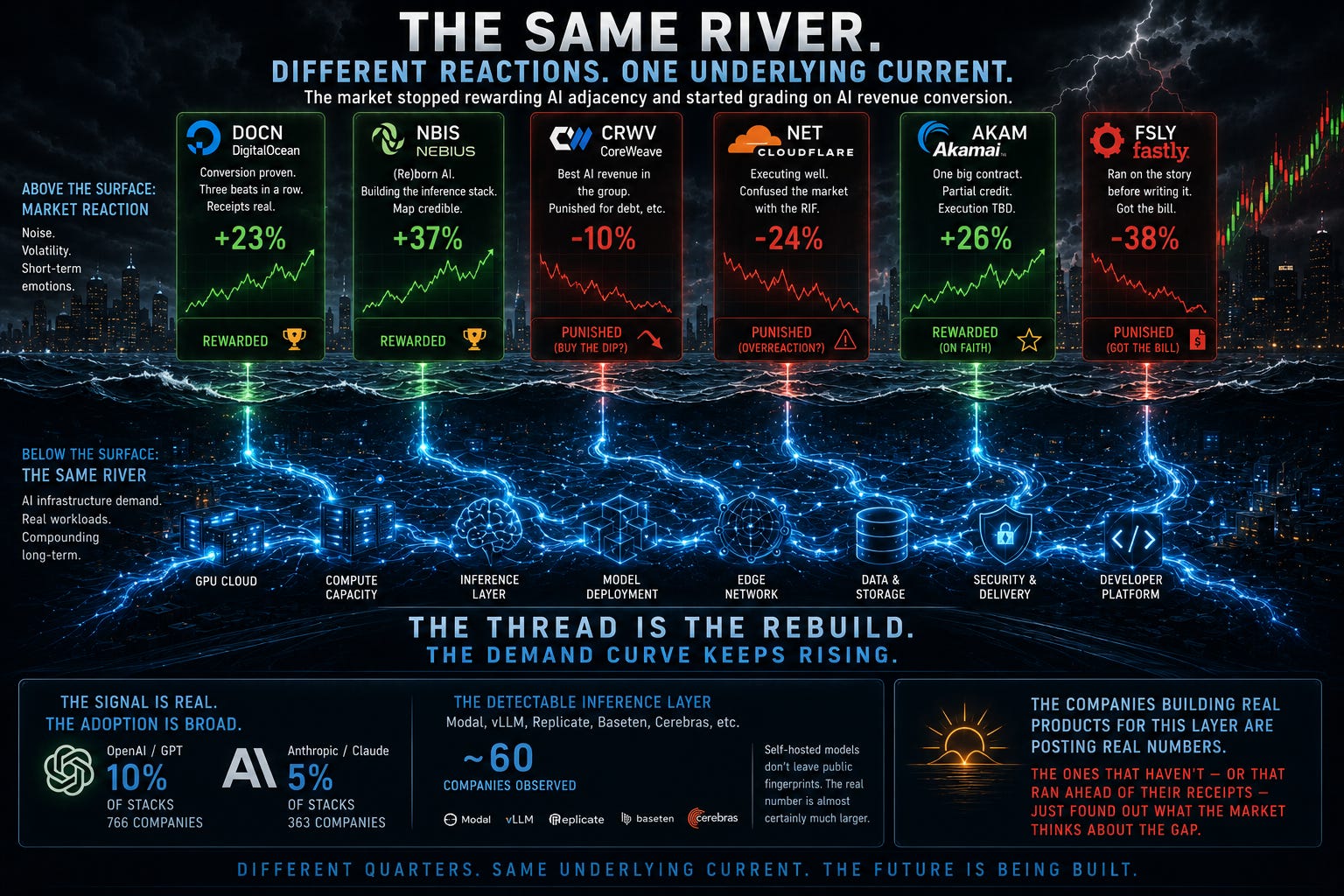

Six stocks. Most beat. One pattern.

The market stopped rewarding AI adjacency and started grading on AI revenue conversion. How complete is your pivot? How real are the receipts? How much rope do you have while we wait?

DOCN: conversion proven, three beats in a row, receipts real → rewarded. ✅

NBIS: (re)born AI, building the inference stack, map credible → rewarded. ✅

CRWV: best AI revenue in the group, punished for debt etc. → punished (buy the dip). 🤦♂️

NET: executing well, confused the market with the RIF → punished (overreaction?) 🤮

AKAM: one big contract, partial credit, execution TBD → rewarded (on faith). ✅

FSLY: ran on the story before writing it → punished (i.e., got the bill). 📉

From STAX: across 10K+ VC-backed companies, OpenAI/GPT appears in 10% of stacks (766 companies), Anthropic/Claude in 5% (363). The detectable inference layer — Modal, vLLM, Replicate, Baseten, Cerebras — is still only ~60 companies in total. Self-hosted models don’t leave public fingerprints, so the real number is almost certainly much larger. But even that small signal is compounding.

The companies building real products for this layer are starting to post real numbers. The ones that haven’t — or that ran ahead of their receipts — just found out what the market thinks about the gap.

Zoom out.

Here’s the thing about this volatility: none of it changes the trade.

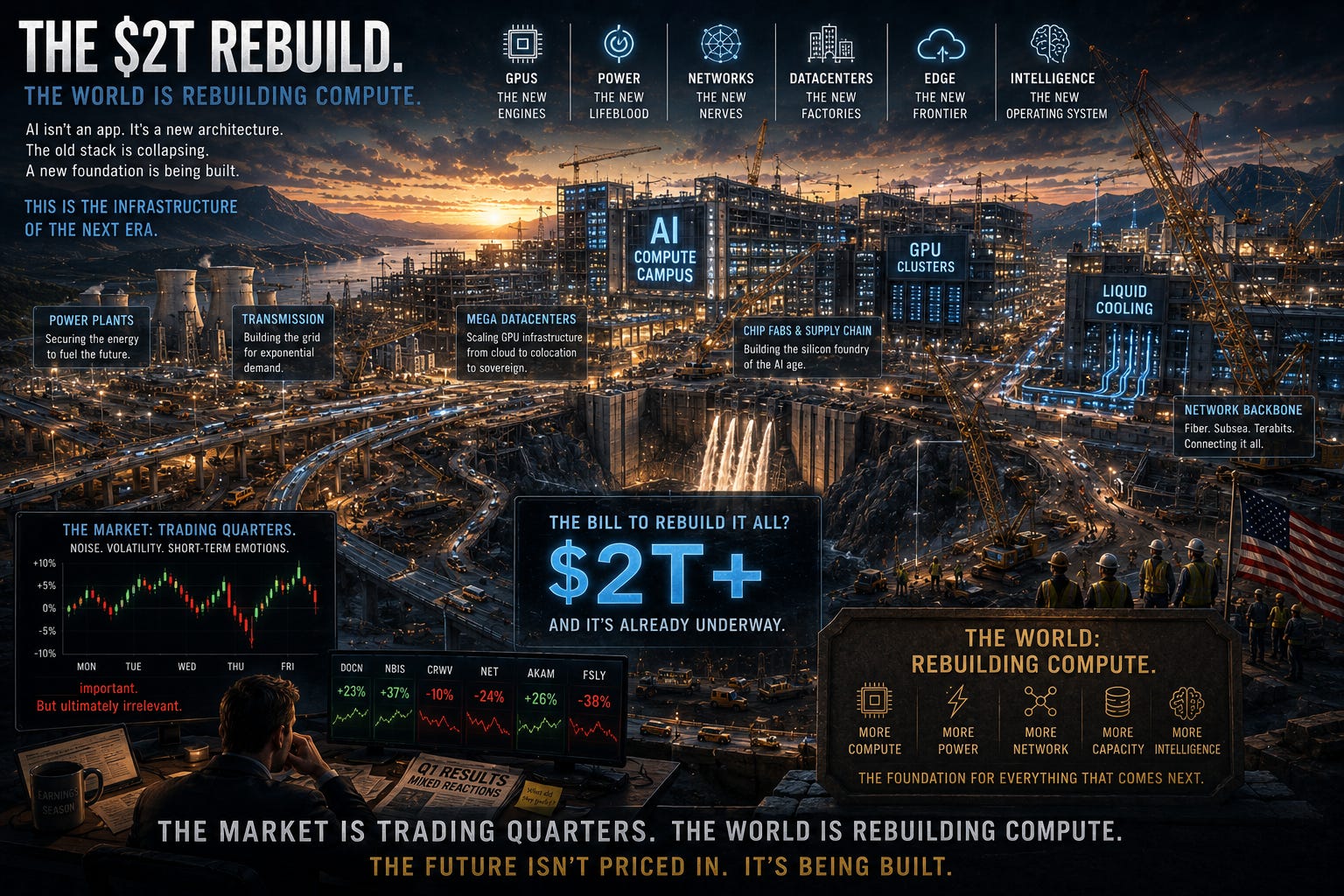

In February 2024 — before CRWV went public, DOCN found AI religion, and most people thought the word “neocloud” meant some sort of toilet paper — I laid out this thesis: the entire world’s computing infrastructure has to be rebuilt.

The reason: AI isn’t just a new application running on top of existing infrastructure. It’s a new architecture that replaces it. The traditional three-tier stack — frontend, logic, database — is collapsing into a single layer. The LLM is the logic and the database and (increasingly) the front-end. And that single layer runs on GPUs.

The bill to rebuild it is probably $2T+ and, while the hyperscalers will capture a lot of it, the gap is too big and expensive (and they’re going to be too slow and too general-purpose and they have their own $250B+ in legacy revenue to support) for the companies that need to run AI workloads at speed and at scale. That gap is exactly why the neocloud thesis exists. That gap is CRWV and NBIS, and it’s what DOCN is building toward and why AKAM just got a $1.8B vote of confidence.

This week’s earnings were a broader check-in on the thesis. The direction, for the companies with real proof, is not in question.

The trade, From the Porch.

The market is now moving on proof — so it’s going to be bumpy. Beat-and-punish quarters. Guidance-miss selloffs. RIF announcements that spook people who aren’t reading them right. Along with waking up to smart deals you didn’t expect that light a fire under your position. That is and was always the price of admission.

None of the volatility changed what these companies are building or what the demand curve looks like.

DOCN and NBIS have the receipts. Hold them. Add on weakness.

CRWV is the most frustrating stock in this group and probably the most important company. Three consecutive beat-and-punish quarters and the backlog is almost $100B. The capital structure is, well, anxiety-inducing, but the demand is not. If you have a long enough time horizon, the dip is a gift. (I’m buying.)

NET is doing the right things and got punished for saying so too loudly. That usually corrects.

AKAM is interesting now in a way it wasn’t last month. One contract isn’t a thesis, but it’s a first receipt. Watch.

FSLY is the cautionary tale, not the opportunity. The stock ran on narrative. The narrative is unproven. Maybe they get there. But “maybe” isn’t the standard the market is applying anymore.

Every week that passes with more AI workloads running in production is another week where the infrastructure underneath them gets more essential and more defensible.

The market is trading quarters while the world is rebuilding compute. The stock charts will be bumpy, but the infrastructure layer for AI will be worth the ride.

Disclosed long positions: CRWV, NBIS, NVDA. Nothing here is investment advice. Do your own work.